Whether you're a sole-trader sparkie, a plumber stepping up from one ute to a small fleet, or a multi-trade business running plumbing, electrical and carpentry crews, the tools of your trade cost money — and tying up your cash to buy them outright can stall your growth. Tradie finance lets you spread the cost of the vehicles, equipment and working capital your business needs, while keeping cash free for materials, wages and the next job.

This guide covers what tradies can finance, the loan structures available, how approvals work (including low doc and new-ABN options), the tax angle, and how to make sure you're getting the sharpest rate.

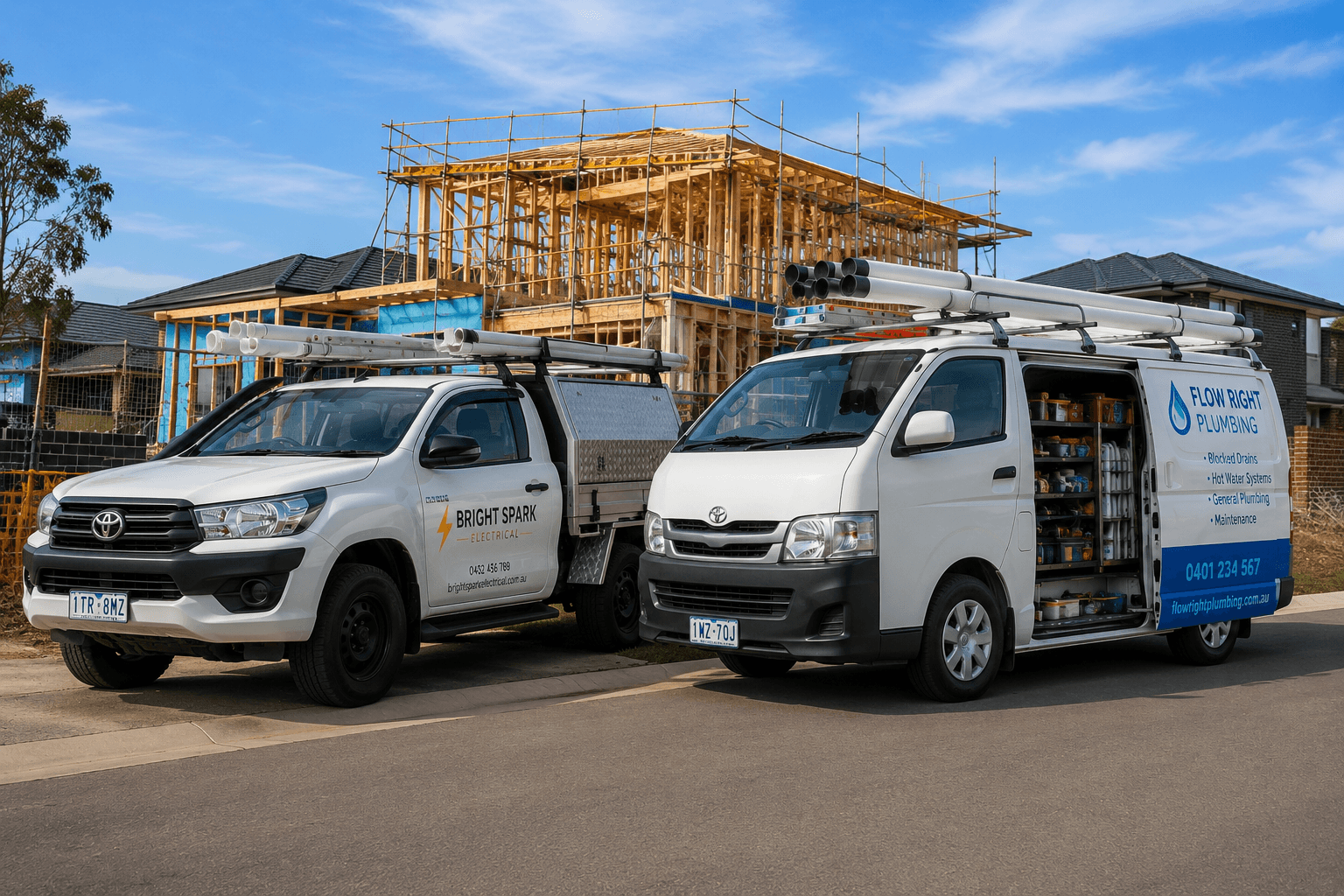

What can tradies finance?

If it helps you earn a living on the tools, it can usually be financed. The most common assets we arrange finance for include:

- Work utes and dual-cabs — Toyota HiLux, Ford Ranger, Isuzu D-MAX, Mitsubishi Triton and more

- Work vans and fitted-out mobile workshops

- Light and heavy trucks, tippers and tray trucks

- Box, tipper, plant and enclosed trailers

- Tools, power equipment and workshop machinery

- Mini excavators, skid steers, compactors and light site plant

- Scissor lifts, boom lifts and other EWPs for access work

- Business and cash flow loans for materials, wages and expansion

Finance structures for tradies

The right structure depends on your tax position, cash flow and whether you want to own the asset outright. The main options are:

- Chattel mortgage — you own the asset from day one while the lender holds it as security. You can typically claim the GST on the purchase and depreciate the asset. The most popular structure for established trade businesses.

- Commercial hire purchase — the lender owns the asset until the final payment, then ownership transfers to you. Useful for managing GST and cash flow.

- Finance lease — the lender owns the asset and you pay to use it, with an optional residual at the end. Handy for fleets managed on a turnover cycle.

- Rent-to-own — flexible option that can suit newer businesses or those building their credit profile.

Low doc and new-ABN approvals

Banks often want two years of full financials and lean heavily on your personal credit score — which is exactly where a lot of tradies get knocked back, especially if you're newly self-employed or your income moves with the job book. Specialist lenders assess your ABN, BAS and the asset itself, so approvals are faster and more flexible.

Low doc finance is available up to $500,000 on the strength of your ABN, licence and bank statements — no full tax returns required. And you don't need years of trading history: we work with lenders who fund brand-new and even 1-day ABNs, with approval based on the asset, your deposit or trade-in, and your credit profile.

Do I need a deposit or property?

Not necessarily. $0 deposit options are available for eligible trade businesses — particularly asset-backed operators with around two years of GST registration. You also don't need to own property: many lenders secure the loan against the asset itself rather than your home, so non-property owners are regularly approved.

The tax angle

Financing your work vehicle or equipment through the right structure can deliver real tax benefits. A chattel mortgage can let you claim the GST on the purchase price and depreciate the asset over time, and eligible assets may qualify for the instant asset write-off. The rules and thresholds change, so always confirm the details with your accountant for your specific circumstances — but for most tradies, financing is more tax-effective than paying cash.

Business and cash flow loans

Tradie finance isn't just about vehicles and equipment. If you're waiting 30 to 60 days to get paid while wages and material costs roll in, a business or cash flow loan can bridge the gap and keep jobs moving. These are typically assessed on your turnover and bank statements, with fast approvals for established ABN holders.

How to get the best deal

Never rely on a verbal rate from a dealer — always get the quote in writing so you can compare the true cost, including fees and charges. The rate you're offered depends on the asset, your ABN history, your credit profile and the lender's appetite, and it can vary significantly from one lender to the next. That's where a broker earns its keep: rather than being stuck with one bank's rate card, we compare 80+ lenders in a single application to find the lender best suited to your deal.

Why use a finance broker?

At Overdrive Funding, we work for you, not the bank. We assess your ABN, BAS and job book to match you with the right lender, negotiate a competitive rate, handle the paperwork end to end, and coordinate settlement with the dealer, private seller or auction house. One application, multiple options, and a pre-approval valid for 90 days so you can buy with confidence.

Can sole traders, apprentices and casuals get approved?

Yes — being self-employed doesn't rule you out, it just changes which lender is the right fit. Sole traders, subcontractors, partnerships, companies and trusts can all be financed, and lenders assess each a little differently based on ABN history, income evidence and the asset. Apprentices and casual workers can also have options; because income can be lower or variable, lenders look more closely at consistency, employment history and affordability, and a deposit or a slightly smaller loan can strengthen the application. The key is matching your profile to a lender who understands it — which is exactly what a broker does for you.

Common roadblocks (and how to get around them)

Most declined tradie deals fall over for avoidable reasons. The good news is that with the right lender and a bit of preparation, they're usually fixable:

- Messy paperwork — missing BAS, mixed personal and business accounts, or out-of-date figures. Tidy records make approval faster.

- New ABN — not a deal breaker, but it needs the right lender and realistic expectations on deposit and rate.

- Tax returns behind — some lenders don't need them at all; knowing which ones to approach is half the battle.

- Bank knock-backs — banks use rigid credit templates; specialist lenders look at the full picture of your trade business.

- Using personal loans or credit cards for work gear — usually more expensive and harder on your cash flow than proper asset finance.

How to give yourself the best shot at approval

- Have the invoice or quote for the asset ready

- Know whether it's for business or personal use

- Confirm your ABN and GST details

- Have recent BAS or bank statements on hand for a low-doc deal

- Check your credit history before you apply

- Be clear on any deposit or trade-in you can put in

- Let us compare lenders first, so your application only goes to the right one — avoiding unnecessary credit enquiries

Tradie finance FAQs

Can I finance a second-hand ute? Yes — many lenders finance used vehicles, including older models, depending on condition and value. Can I finance a private sale? Yes, though deposits and checks are usually a little higher than a dealer purchase. Can I finance tools only? Often yes, depending on the value and lender — tool and equipment packages are common. Can I get approved with bad credit? Possibly — a past default doesn't automatically mean no, it just changes the lender and the structure. How fast is approval? Once we've reviewed your documents, some approvals come through the same day, with pre-approval typically inside 24 to 48 hours.

Ready to get your next ute, van, truck or piece of equipment on the road? Explore our tradie finance options, or get in touch with Simon and the team for a free, no-obligation quote and see how much you could save on your tradie finance.